B2B cash flow rarely moves in a straight line. Stocking up ahead of a seasonal spike, juggling supplier terms while customer payments clear, or ramping up for a new project can all create timing gaps. This Australia-focused guide explains how a merchant cash advance works for B2B businesses. Learn how repayments are typically taken from EFTPOS and online card sales, and what it can be worth comparing when reviewing providers.

What A Merchant Cash Advance Is

A merchant cash advance is a form of business funding in which a provider pays an upfront amount in exchange for an agreed share of future card sales, such as EFTPOS and online card transactions.

Rather than fixed monthly instalments, repayments are typically collected automatically as a percentage of card transactions. So the repayment amount usually rises and falls with card revenue.

Structurally, that’s different from a standard term loan. A term loan normally has set repayments on a schedule. It also has pricing quoted as an interest rate plus fees.

For B2B businesses, it can be relevant when customers pay by card for deposits, online checkout, subscriptions, or smaller repeat orders.

It often suits situations where card turnover is a meaningful part of overall revenue.

How A Merchant Cash Advance Typically Works

A merchant cash advance typically starts with an application and a review of recent EFTPOS and online card turnover. Businesses will then receive an upfront advance. MCA providers will take automatic repayments from card takings until the agreed total is repaid.

The Repayment “Holdback” And How Deductions Happen

Repayments are typically collected through a “holdback”, which is a fixed percentage of your card sales.

When a customer pays by card, that percentage is usually deducted automatically and forwarded to the provider. Or it may be calculated and deducted daily, depending on how your payment processing is set up.

For example, with a 10% holdback, $10 from every $100 in card sales would typically go toward repayment.

Because it’s tied to card takings, the deductions are often easy to see alongside your EFTPOS and online transaction reporting.

Why Repayments Can Feel Different Month To Month

Since the holdback is a percentage, repayments typically rise and fall with sales volume.

In busier months, higher card turnover usually means larger deductions, so the balance may reduce more quickly.

However, in quieter periods, lower card takings generally mean smaller deductions. This can make cash flow feel less tight than a fixed repayment schedule.

This flexibility can suit businesses with seasonal patterns or project-based spikes.

Because repayments often track more closely with revenue as it comes in.

At the same time, the repayment pace can vary, so the end date is usually less predictable than with set instalments.

Costs, Fees, And The Real Price Of the Advance

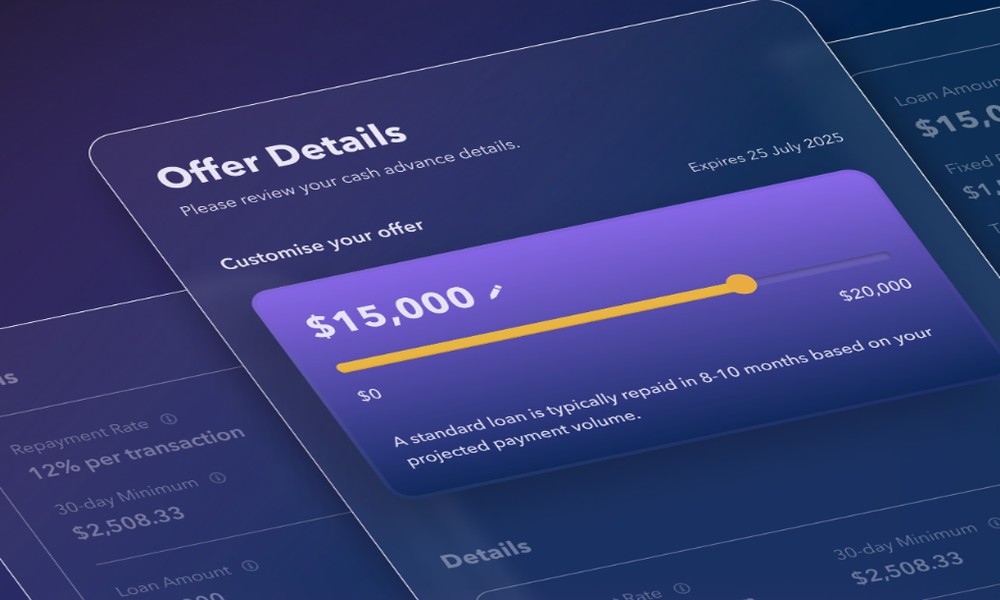

When describing pricing, it typically helps to centre on two numbers: the upfront amount received and the total amount repaid.

A merchant cash advance is often priced differently from a standard term loan, which usually shows an interest rate and set repayments. Instead, providers commonly use a fixed fee to calculate the total repayable amount at the start.

Repayments are then collected as a percentage of EFTPOS and online card takings. So the timeframe can vary with sales, even when the total payback is agreed upfront.

When A Merchant Cash Advance May Be Considered For B2B Growth Periods

A merchant cash advance may suit some B2B businesses when timing is a key factor. Businesses going through expansion phase, seasonal peaks, or other high-activity periods typically benefit from added flexibility.

Common Opportunity-Driven Use Cases

In B2B settings, a merchant cash advance could be used to bring stock in ahead of a busy season. Businesses can also take advantage of supplier pre-pay discounts, or support a marketing push for a new product line.

MCA may also suit equipment upgrades that increase capacity, or hiring and onboarding costs linked to an anticipated contract.

For businesses with predictable peak periods, it can help smooth working capital timing as revenue builds.

Good Fit Indicators

It typically aligns best with businesses that have consistent card turnover through EFTPOS or online payments and fairly predictable sales patterns.

Repayments are usually collected as a percentage of card takings. Therefore, it can be helpful if day-to-day cash flow has enough room to absorb variable deductions without putting pressure on regular operating costs.

It’s often a better fit when card revenue is a meaningful channel, even if the business also relies on invoicing and bank transfers for larger accounts.

Potential Advantages And Trade-offs

A merchant cash advance can suit some B2B businesses when timing matters and card sales make up a meaningful share of turnover.

One potential advantage is speed. Assessment can move faster than some traditional pathways when recent EFTPOS and online transaction history is a key input.

Repayments can also feel more flexible, because deductions typically rise and fall with card takings rather than staying fixed each month.

Moreover, the application may be relatively straightforward for businesses with steady card turnover.

However, there are trade-offs to weigh as well. The effective cost can be higher in many cases, especially when pricing is set through a factor rate or fixed fee.

Additionally, the end date is often less predictable because repayment speed depends on sales volume. Daily or per-transaction deductions can affect cash flow planning around payroll, supplier payments, and inventory purchases.

Comparing A Merchant Cash Advance With Other Business Funding Options

It’s usually helpful to compare how different business funding structures are priced and repaid. Businesses should also evaluate cash flow timing and repayment predictability.

Merchant Cash Advance Vs Business Loan (High-Level)

A business loan typically has a set term with scheduled repayments (weekly or monthly) and pricing expressed as an interest rate plus fees. This can make budgeting more predictable.

However, a merchant cash advance works differently. Repayments are usually taken as a percentage of EFTPOS and online card takings. Pricing is often set via a factor rate or fixed fee that determines the total repayable upfront. Because deductions move with sales, the timeframe can be less certain.

Merchant Cash Advance Vs Business Line Of Credit (High-Level)

A business line of credit typically provides access to funds up to a limit. As you repay, the available credit can usually be reused (subject to terms), which can accommodate flexible, smaller drawdowns over time.

In contrast, a merchant cash advance is usually a one-off amount. This amount is repaid automatically from EFTPOS and online card takings until the agreed total is cleared. The core difference is reuse and drawdown control versus a single advance tied to card turnover.

What To Check Before Choosing Any Provider

Before committing to any provider, it’s important to review the key terms in a way that matches how your business typically manages cash flow during growth periods and seasonal swings:

- Total Repayable Amount: Confirm the total repayable figure (not just the upfront advance) so comparisons are like-for-like.

- Holdback Percentage: Check the percentage deducted from EFTPOS and online card takings. Consider how it may feel in quieter weeks versus peak trading.

- Additional Fees And Charges: Look for establishment fees, ongoing fees, early payout costs, or other charges that could change the overall price.

- How Deductions Are Calculated: Clarify whether repayments are taken per transaction or settled daily. Determine whether the holdback applies to gross card takings or another method.

- Which Card Channels Apply: Confirm whether deductions apply across in-store EFTPOS, online payments, and recurring billing, or only specific terminals or processors.

- Payment Processing Changes: Ask what happens if you switch payment providers, add new terminals, or shift sales channels. Make sure you know whether that affects how repayments are collected.

Conclusion

A merchant cash advance provides an upfront amount in exchange for an agreed share of future EFTPOS and online card takings.

Repayments are typically collected automatically as a percentage of card sales. So deductions usually rise and fall with turnover, which can align with seasonal peaks or growth-related spikes.

Since pricing is often set through a factor rate or fixed fee, the total repayable amount is just as important as the amount received.

Just keep in mind that the fit often comes down to how meaningful card turnover is for your business and how your cash flow timing shifts across the year. It can be worth comparing fees and repayment mechanics carefully.