Every mobile retailer offering EMI-based sales in India eventually faces the same problem – what happens when a customer stops paying? For years, the answer was traditional debt recovery: phone calls, field agents, legal notices, and long waiting periods. Today, a growing number of retailers and lending partners are turning to device locking as a faster, leaner alternative. But which approach actually delivers better results on the ground?

The Real Cost of Traditional Debt Recovery

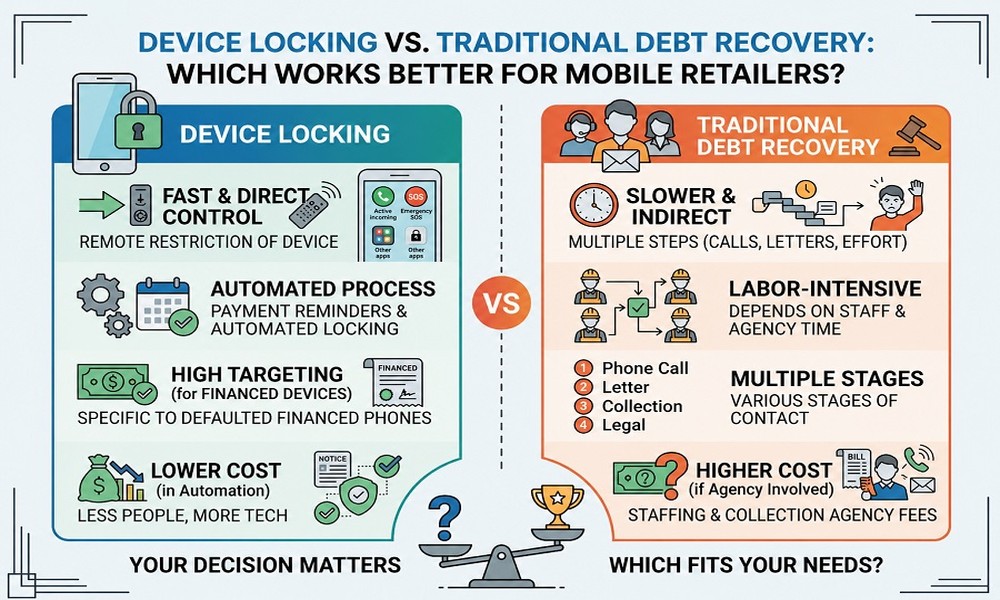

Traditional debt recovery is labour-intensive by nature. When a customer defaults, the process begins with repeated phone calls, escalates to field visits, and in serious cases, moves toward legal action. Each step costs money, time, and manpower.

For mobile retailers operating on thin margins – which is most of them – this model is difficult to sustain. A single default case involving a handset worth ₹15,000 can consume more in recovery costs than the outstanding amount itself. Add the inconsistency in outcomes, the friction of confrontational recovery, and the reputational risk of aggressive tactics, and traditional debt recovery starts to look like a very expensive gamble.

How Device Locking Changes the Equation

Device locking flips the recovery dynamic entirely. Instead of chasing a defaulter after the fact, the lender already holds leverage from day one – the phone itself. A device locking system embedded in the handset allows the retailer or financing partner to remotely restrict the phone’s functionality when a payment is missed, without a single field visit.

The impact is significant. When a customer knows that missing an EMI will render their phone unusable, the motivation to pay on time increases sharply. Device locking does not just recover debt – it prevents default from escalating in the first place.

For retailers, this means lower operational costs, reduced dependence on recovery agents, and faster resolution. A lock can be triggered within hours of a missed payment and lifted just as quickly once dues are cleared.

Where Traditional Recovery Still Holds Ground

Device locking is not a universal fix. Older or low-end devices often lack the software compatibility required for these systems. In such cases, retailers have no choice but to fall back on conventional methods. For large outstanding amounts – say, a premium device financed over 24 months – legal recovery may still be necessary even after a lock is in place.

There is also a human element that technology cannot fully replace. Experienced recovery agents can negotiate restructured payment plans and assess genuine financial hardship – judgment calls that an automated system simply cannot make.

Comparing the Two

Device locking wins on speed, cost-efficiency, and scalability. It requires no field agents, generates no confrontation, and works around the clock. For early-stage defaults on mid-range handsets – the bulk of EMI sales in India – it is clearly the more effective tool.

Traditional debt recovery wins on flexibility. It remains necessary for complex or high-value cases where a lock alone is not enough to resolve the situation.

Conclusion

For mobile retailers in India, device locking represents a meaningful step forward over traditional debt recovery – particularly for managing early defaults at scale. It is faster, cheaper, and far less operationally demanding. That said, the smartest retailers are not choosing one over the other. They are using device locking as the first line of defence and keeping traditional recovery as a fallback for cases where technology alone cannot close the loop.